Table Of Content

Generally speaking, most prospective homeowners can afford to finance a property whose mortgage is between two and two-and-a-half times their annual gross income. Under this formula, a person earning $100,000 per year can only afford a mortgage of $200,000 to $250,000. Only 25 percent could afford the purchase, the association found, up from 22 percent at this time last year.

Calculate mortgage rates

Calculate the home price you can pay and the mortgage schedule you will need based on the payment, down payment, taxes and insurance you can afford. This calculator should give you a rough idea of your house price range based on the monthly payment you can afford for a mortgage. Once you are ready, you'll need to get professional mortgage advice on your actual affordability. Other factors include your credit rating and fees that you pay up front or roll into the mortgage loan. Spend some time thinking about how much money you can afford to spend on your monthly mortgage payments.

Housing market: Who can afford to buy a home these days? – Deseret News - Deseret News

Housing market: Who can afford to buy a home these days? – Deseret News.

Posted: Fri, 20 Oct 2023 07:00:00 GMT [source]

Front-End Ratio

But they’ll charge you higher interest rates and add extra fees like mortgage insurance to protect themselves (not you) in case you get in over your head and can’t make your mortgage payments. Also known as the debt-to-income ratio (DTI), it calculates the percentage of your gross income required to cover your debts. Debts include credit card payments, child support, and other outstanding loans (auto, student, etc.).

Association Fees

If you only consider the price of your home, you’re missing out on a big part of the financial picture. When you figure out your total monthly household income, be sure to consider any recurring debt and expenses. For instance, if you want a lower monthly payment then you’ll want to choose a 30-year loan term. If you’re looking to pay less money in interest overall and can manage a higher monthly payment, you’ll want to choose a shorter loan term. You can calculate your down payment as either a percentage or a flat dollar amount using the Rocket Mortgage calculator.

Just 15% of Californians can afford a home, lowest rate in 16 years - OCRegister

Just 15% of Californians can afford a home, lowest rate in 16 years.

Posted: Fri, 10 Nov 2023 08:00:00 GMT [source]

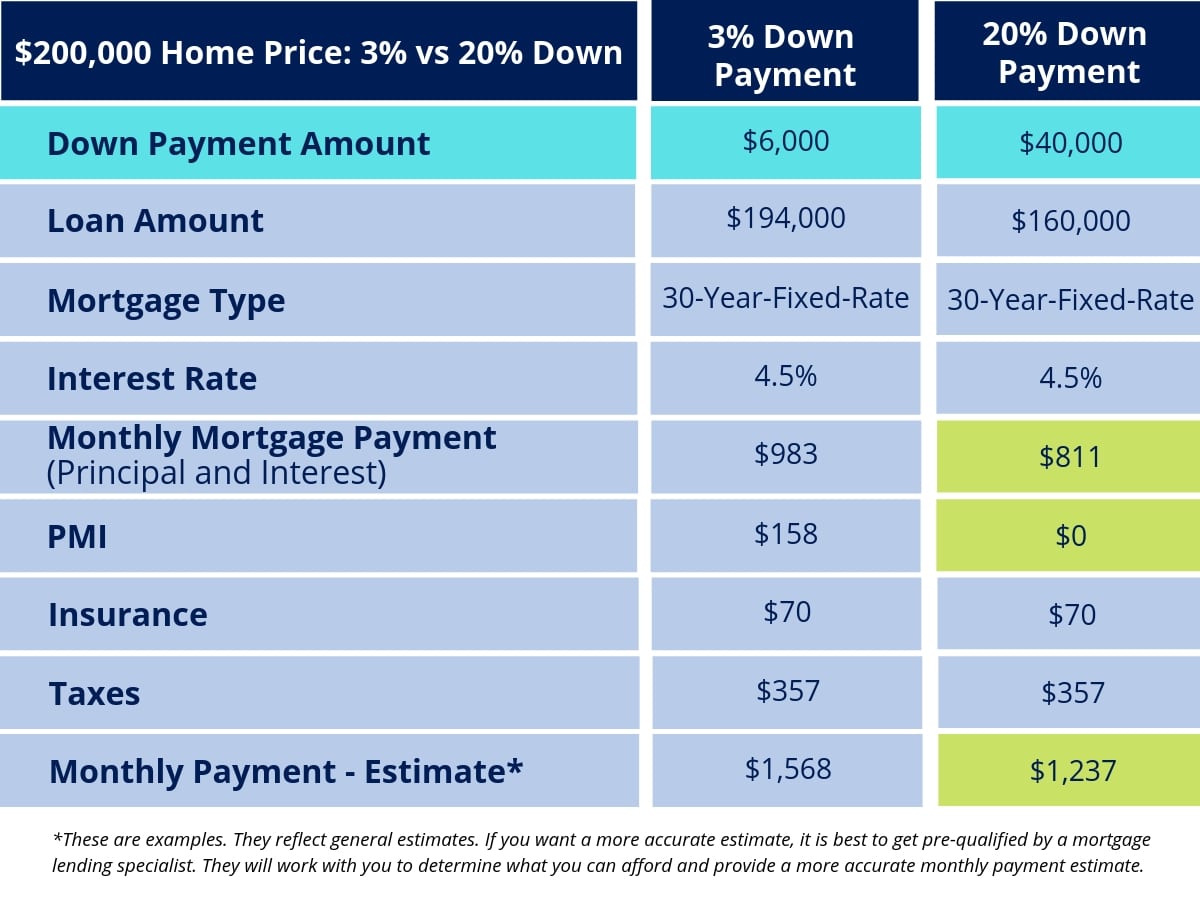

It only makes sense to make a large down payment if you have a lot of cash on hand and would like to avoid paying PMI or reduce your monthly payments. If making a large down payment would erase your financial reserves for future emergencies, then this is not a good idea. There are no set rules regarding how much of your income should cover a mortgage payment. However, lenders will look at how much of your income is going to other outstanding debts before approving another loan. Check out this guide for the different methods for determining how much of your income should go to your mortgage.

Los Angeles Real Estate Market Reports

Just because a lender is willing to give you money for a home doesn’t necessarily mean that you have to jump into homeownership. It’s a big responsibility that ties up a large amount of money for years. But beyond that you’ve got to think about your lifestyle, such as how much money you have leftover for travel, retirement, other financial goals, etc. You might find that you don’t want to buy the most expensive home that fits in your budget. Banks don’t like to lend to borrowers who have a low margin of error.

Other Factors That Influence How Much House You Can Afford

You will have an easier time making your payments, or (better yet!) you will be able to pay extra on the principal and save yourself money by paying off your mortgage early. Even though Martin can technically afford House #2 and Teresa can technically afford House #3, both of them may decide not to. If Martin waits another year to buy, he can use some of his high income to save for a larger down payment. Teresa may want to find a slightly cheaper home so she’s not right at that maximum of paying 36% of her pre-tax income toward debt.

The calculator also allows the user to select from debt-to-income ratios between 10% to 50% in increments of 5%. If coupled with down payments less than 20%, 0.5% of PMI insurance will automatically be added to monthly housing costs because they are assumed to be calculations for conventional loans. There are no options above 50% because that is the point at which DTI exceeds risk thresholds for nearly all mortgage lenders.

Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers. Along the same lines of thinking, you might consider holding off on buying the house.

For instance, a 4% interest rate means you’ll pay 4% on the total loan balance until the mortgage is paid off. We’ll check your credit history to give you an even more solid estimate of what you can afford, along with your expected rate and monthly payment. Once again, the answer to this question will depend on where you want to buy and what kind of property you want. Your credit score and DTI will also be important factors in determining what interest rate and loan terms you get from the lender. Fees depend on how many amenities the community has, how many services it requires, and how much upkeep it needs.

You might not spend this amount each year, but you’ll spend it eventually. We’ll walk you through how to calculate how much home you can afford in more detail. On mobile devices, tap "Refine Results" to find the field to enter the rate and use the plus and minus signs to select the "Loan term." Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens.

No comments:

Post a Comment